California SB 253 Deadline Approaching: Why August 2026 Is Your Last Chance to Prepare (And What Happens If You Don't)

16 FEB 2026

•

9 MIN READ

Introduction

Six months. That's all the time between you and California's most aggressive climate disclosure deadline. And if you're just starting now, you're in trouble.

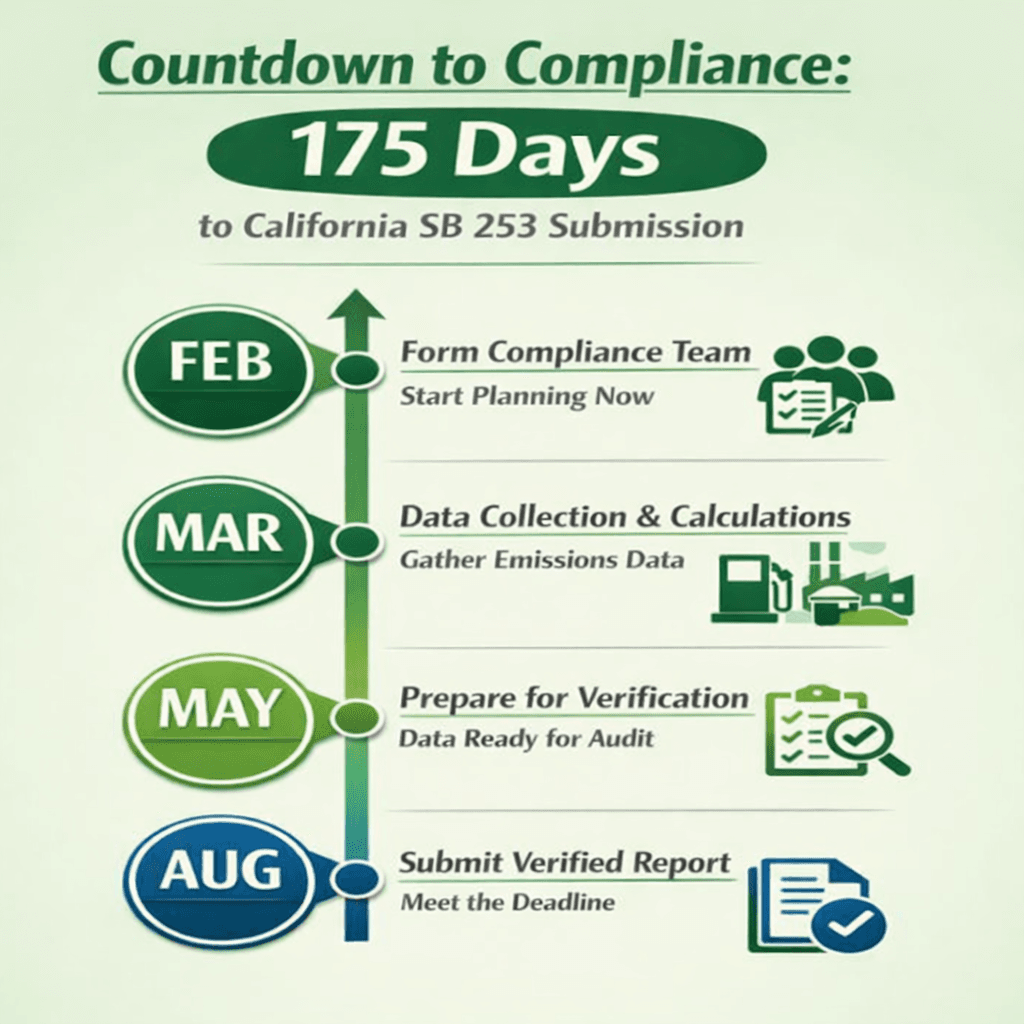

Here's a number that should terrify you : 175 days.

That's approximately how much time remains until August 2026, when California SB 253 mandates that every company doing business in the state with over $1 billion in annual revenue must submit their first independently verified greenhouse gas emissions report.

Not a voluntary sustainability summary. Not a marketing document. A mandatory, third-party audited disclosure that meets specific technical standards under the GHG Protocol.

And here's the part that makes compliance officers lose sleep: the third-party verification process alone takes 60-90 days minimum. That means your emissions data needs to be complete, organized, and calculation-ready by May 2026—roughly 75 days from today.

Download: California SB 253 – 6-Month Compliance Roadmap (Mid Feb–Aug 2026)

A week-by-week, verification-ready action plan covering data collection, calculations, documentation, and third-party verification timelines.

Download the PDFIf you're reading this and thinking 'we'll figure it out,' let me stop you right there. This isn't a problem you can solve with a last-minute sprint. This is infrastructure you should have started building 18 months ago.

But you didn't. And now you're here.

What Makes SB 253 Different (And Why It's Catching Companies Off Guard)

Most environmental reporting allows for self-certification or internal audits. SB 253 doesn't. It requires independent verification by accredited third parties who will scrutinize your data with the same rigor as a financial audit.

Here's what that actually means in practice:

Your verifier will examine every emission source you've reported. They'll demand documentation for every number—utility bills, fuel receipts, meter readings, service records. They'll check your calculation methodologies against established GHG Protocol standards. They'll interview the people who collected your data. They'll test your assumptions and quality assurance processes.

If they find gaps, inconsistencies, or unsupported estimates, they won't give you a gentle warning. They'll issue a qualified opinion or refuse to verify entirely.

And without verification, your report doesn't count.

The verification firms taking on SB 253 engagements are serious operations—think environmental divisions of major accounting firms, specialized climate auditors, and accredited verification bodies. They're not in the business of rubber-stamping questionable data.

The Data Infrastructure Problem Most Companies Don't Have

Your organization has been doing financial accounting for decades. You have sophisticated systems, established processes, trained personnel, and clear audit trails for tracking every dollar.

Now imagine trying to build that same level of rigor for emissions accounting in six months.

That's the challenge.

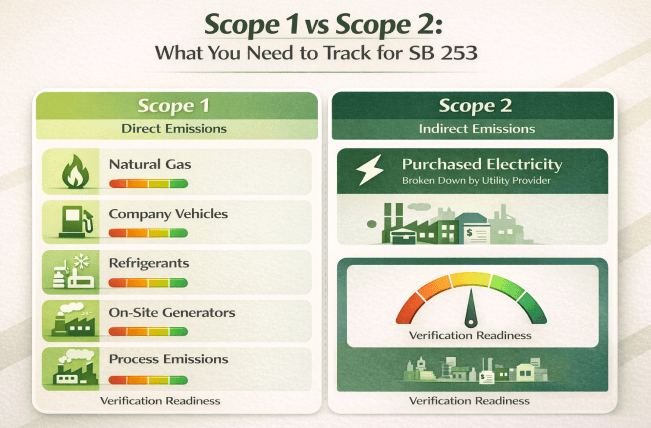

SB 253 requires reporting on Scope 1 emissions (direct emissions from sources you own or control) and Scope 2 emissions (indirect emissions from purchased electricity). This sounds straightforward until you start inventorying actual emission sources:

Scope 1 includes:

- Natural gas consumption at every facility

- Diesel, gasoline, and propane used across all operations

- Company vehicle fuel consumption

- Fugitive emissions from refrigerants and HVAC systems

- On-site generators and emergency backup systems

- Process emissions from manufacturing operations

Scope 2 includes:

- Purchased electricity at every location

- Data broken down by utility provider

- Consumption data that allows for both location-based and market-based calculations

Now consider the practical reality: If you operate 50 locations across California, you're dealing with dozens of utility accounts, multiple landlord relationships (for leased spaces), several fuel suppliers, various vehicle fleets, and scattered facilities teams using different systems to track consumption.

Getting clean, verifiable data from all these sources isn't a project you complete in a weekend. It's infrastructure you build over months.

The Common Obstacles That Are Derailing Compliance Efforts

As of mid-February 2026, companies subject to SB 253 are running into predictable problems that are proving harder to solve than expected.

Data Access Issues That Can't Be Solved Quickly

The Leased Space Problem:

Many companies operate in buildings they don't own. In these cases, landlords often pay utilities directly. Getting detailed consumption data requires cooperation from property management companies who aren't legally required to provide granular energy usage information. Even willing landlords often don't have data in the format needed for emissions calculations.

The Utility Provider Challenge:

Accessing historical consumption data isn't always straightforward. Some utility providers require formal authorization processes. Others have customer portals with limited historical data access. Companies that switched providers during the reporting period often discover that accessing data from previous providers requires time-consuming data requests.

The Multi-Location Complexity:

Organizations with numerous facilities face a coordination nightmare. Each location may have different utility providers, different facilities managers with varying data management practices, and different systems for tracking consumption. Aggregating this data consistently across locations requires standardized processes that many companies don't have.

The Documentation Gap That Kills Verification

Verifiers don't just want your final numbers—they want to see the evidence trail. This means:

- Original source documents (utility bills, fuel invoices, meter readings)

- Clear calculation worksheets showing methodology

- Documented emission factors with source citations

- Explanation of any estimation methods used

- Quality assurance processes demonstrating data accuracy

Many companies have been tracking some emissions data but without maintaining proper documentation. They have numbers in spreadsheets but can't prove where those numbers came from or how they were calculated. During verification, this becomes a fatal problem.

The Refrigerant Tracking Blind Spot

Fugitive emissions from refrigerants often represent a significant portion of Scope 1 emissions, yet most facilities teams don't systematically track refrigerant usage. Getting this data requires:

- Identifying all equipment containing refrigerants

- Knowing what type of refrigerant each system uses

- Tracking refrigerant additions during service calls

- Estimating leakage rates

- Obtaining documentation from HVAC contractors

Service records are often scattered across multiple contractors, filed inconsistently, or maintained only as handwritten work orders. Reconstructing a full year of refrigerant data from these sources is tedious detective work.

The Methodology Selection Dilemma

The GHG Protocol offers multiple calculation approaches for certain emission sources. Choosing the wrong methodology or mixing methodologies inappropriately can result in verification failure.

For Scope 2 emissions, companies must report using both the location-based method (based on average grid emissions) and the market-based method (accounting for specific electricity products purchased). Many companies initially calculated using only one method, requiring complete recalculation.

Emission factors—the coefficients used to convert activity data into emissions—must come from recognized sources and must be appropriate for the reporting period and geographic location. Using outdated factors or national averages when California-specific factors are available creates verification issues.

What Actually Happens If You Miss the August 2026 Deadline

Let's be direct about the consequences of non-compliance, because there's been confusion about what's at stake.

The Regulatory and Financial Exposure

California SB 253 establishes enforcement mechanisms for companies that fail to report or submit reports that don't meet verification standards. While the exact penalty structure has evolved through regulatory guidance, non-compliance carries financial consequences.

Beyond direct penalties, late filing or verification failure triggers additional costs: paying for corrective data collection, conducting additional verification attempts, and managing an extended compliance process while the next reporting cycle approaches.

The Investor and Stakeholder Impact

In August 2026, there will be a clear divide: companies that successfully filed verified reports and companies that didn't.

Investors are increasingly using climate disclosure data to inform decisions. Major institutional investors have publicly committed to considering climate risks in portfolio management. ESG rating agencies incorporate climate disclosure compliance into their assessments.

Companies that comply on time will communicate this through investor relations channels, annual reports, and sustainability communications. The implicit message: we have strong governance, operational maturity, and the capability to meet complex regulatory requirements.

Companies that miss the deadline face uncomfortable questions: Why couldn't you comply with a requirement announced in October 2023? What does this say about your operational capabilities? How will you handle future climate regulations?

The Competitive Positioning Shift

Climate disclosure is becoming a competitive differentiator in multiple ways:

Customer relationships: B2B customers increasingly require suppliers to provide emissions data for their own Scope 3 reporting. Companies with robust climate accounting systems can respond to these requests. Companies without them become less attractive suppliers.

Talent attraction: Particularly in California's tech sector, sustainability credentials matter for recruiting. Employees want to work for companies that take climate seriously. Non-compliance sends a signal.

Supply chain management: As climate regulations expand, companies with strong emissions accounting capabilities have better visibility into their supply chain risks and reduction opportunities.

The Operational Disruption Cycle

Perhaps the most insidious consequence is the crisis cycle that begins with missed deadlines:

You miss the August 2026 deadline, so you're scrambling to file late while simultaneously beginning data collection for the 2026 reporting year. You're perpetually behind, always in reactive mode, never building the systematic processes that would make this manageable.

Meanwhile, the Scope 3 reporting deadline for 2027 approaches. Scope 3 emissions—which cover your entire value chain—are exponentially harder to measure than Scope 1 and 2. Companies barely surviving Scope 1 and 2 reporting face a Scope 3 crisis they're completely unprepared for.

The Scope 3 Reality That's Coming in 2027

Here's what many companies haven't fully processed: August 2026 covers only Scope 1 and Scope 2 emissions. Scope 3 reporting becomes mandatory in 2027.

Scope 3 encompasses your entire value chain—emissions that occur outside your direct operations:

- Purchased goods and services

- Upstream transportation and distribution

- Business travel and employee commuting

- Downstream transportation and distribution

- Use of sold products

- End-of-life treatment

For most companies, Scope 3 represents 70–90% of their total carbon footprint. It's also exponentially harder to measure because it requires data from entities you don't control.

Consider what this means practically: To report Scope 3 emissions from purchased goods, you need emissions data from your suppliers. If you have 500 suppliers, many of whom are small businesses without sophisticated emissions tracking, how do you get that data?

Companies treating SB 253 compliance as a one-time exercise will face the same crisis in 2027 for Scope 3. Companies building systematic emissions accounting infrastructure now will have the foundation to tackle Scope 3 methodically.

What Success Actually Looks Like

Companies that will succeed under SB 253 don’t scramble in 2026—they build for it now. They share a few clear traits:

- They build infrastructure, not one-off projects. Emissions reporting runs continuously, not as an annual fire drill.

- They break silos. Finance, procurement, IT, facilities, and sustainability operate from a shared data system.

- They use the right technology. Automated data capture, standardized calculations, audit trails, and verification-ready reports.

- They partner with verifiers early. Verification is designed in—not bolted on at the end.

- They treat carbon data like financial data. Clear ownership, regular reviews, quality checks, and documented controls.

That’s the difference between checking a box and staying compliant year after year.

The Decision Point You're Facing Right Now

You've reached the end of this blog. You understand the deadline. You understand the challenges. You understand what needs to happen.

Now comes the crucial part: what you actually do.

Because understanding the problem doesn't solve it. Planning to solve it doesn't solve it. Only action solves it.

As of February 16, 2026, you have 175 days until the SB 253 deadline. The verification process takes 60-90 days, meaning your data needs to be ready by May.

That timeline is aggressive but achievable for companies that start immediately and commit resources.

The timeline becomes impossible for companies that spend February planning, March organizing, and April mobilizing. By the time they're actually gathering data, the deadline is too close.

So here's the question: What will you do tomorrow?

Not what will you discuss in next week's meeting. Not what you'll include in next quarter's planning. What specific action will you take on February 17, 2026?

Will you schedule the emergency cross-functional meeting to form your compliance team? Will you send the email to executive leadership outlining the resource requirements? Will you begin the emissions inventory process? Will you research verification firms?

The companies that successfully file verified reports in August 2026 will be the ones that treated mid-February as the start of execution

Why August 2026 Matters More Than You Think

SB 253 isn't happening in isolation. It's part of a broader global movement toward mandatory climate disclosure.

The SEC has proposed climate disclosure rules for public companies. The EU has implemented comprehensive sustainability reporting requirements. Other states are watching California's implementation closely.

Companies that build robust climate accounting capabilities for SB 253 are investing in infrastructure they'll need anyway as disclosure requirements expand. Companies that treat this as minimal compliance will face repeated crises as new regulations emerge.

The question isn't whether your organization needs sophisticated emissions reporting capabilities. The question is whether you'll build them proactively or reactively, with adequate preparation or under crisis conditions.

August 2026 is your forcing function. It's the deadline that makes the abstract concrete. Use it wisely.

Your Next 48 Hours Matter

Here's what separates companies that successfully navigate complex regulatory requirements from those that struggle:

It's not intelligence. It's not resources. It's not even expertise.

It's the ability to recognize when planning needs to stop and execution needs to begin.

Most companies stuck in compliance crisis mode spent months planning instead of doing. They formed committees instead of teams. They created PowerPoint presentations instead of processes. They waited for perfect clarity instead of moving with available information.

You have less than 6 months. That sounds like a lot of time until you map out everything that needs to happen. Then it becomes clear how quickly August will arrive.

The companies making the deadline are the ones taking action right now—today, this week, this month. They're forming teams, inventorying data, engaging verifiers, and treating climate disclosure as the operational priority it needs to be.

The companies that will struggle are the ones still in planning mode in March, still organizing in April, still hoping the problem will somehow become simpler.

California SB 253 compliance is achievable. But not without immediate action. Your last chance to prepare effectively is right now—mid-February is already cutting it close.

SB 253 will not be won by better plans, longer meetings, or clearer guidance. It will be won by companies that start executing now. The next 48 hours won’t feel dramatic—but they will determine whether August is controlled or chaotic.

More Insights

Missed Deadlines, Lost Contracts? How Carbalyze Makes Carbon Reporting Stress-Free

A practical look at how missed deadlines and messy supplier data are costing businesses contracts, and how Carbalyze’s AI-powered platform...

Still Chasing Suppliers for Emission Data? Caly AI Can Fill the Gaps in Minutes, Not Months

Stop chasing suppliers for emission data. Discover how Caly AI turns your BOM into audit-ready Product Carbon Footprints in minutes,...

From Scope 3 to CBAM: Closing the Carbon Data Gap in International Trade

Insights and practical guidance on managing Scope 3 emissions and meeting EU CBAM requirements. Learn how businesses can close carbon...

Fueled by intelligent systems to elevate your reading experience.